Russia invaded Ukraine. It’s all over the news.

The mainstream coverage, rightfully, has been focused on the magnitude of the human tragedy: thousands dead and injured, communities razed, millions displaced and billions of dollars in damage.

Most of the coverage regarding the economic damage has been localized to Ukraine and Russia. How much will it cost to repair Ukraine’s bombed infrastructure and what are the impact of sanctions to Russia’s economy? But, what has largely been ignored, or worse, dismissed, is the impact of Russia’s exit from the world economy, and with it, one of the largest commodity producers in the world.

In the mining industry specifically, the conflict has had a sizeable impact on various parts of the value chain – causing many to be concerned about the downstream effects of further violence and the associated sanctions.

In this article, we’ll explore some of these first and second-order effects in an attempt to ground these concerns more fully. We’ll also look at potential solutions for mitigating some of the damage.

How Is the Mining Industry Affected By the Conflict?

As expected, the impact of such an invasion is wide and varied, but here are some of the key factors impacting the mining industry most seriously:

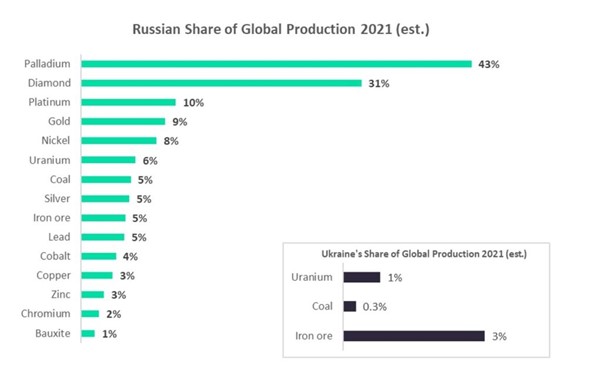

- Raw Material Supply Disruptions. Both Russia and Ukraine are key suppliers of various raw materials that play a significant role throughout the mining value chain. These include palladium, diamond, platinum, nickel, potassium, iron, and numerous others[1]. Palladium is probably the biggest factor here because Russia produces over 40% of the global supply[2]. But the others also represent sizeable chunks of the global market.

Mining companies who were relying on these materials have found their supply disrupted without recourse and it is not clear whether this will return. As such, they have been forced to look for alternative sources to secure the materials needed to run – placing pressure on profitability and their ability to service agreed-upon order volumes.

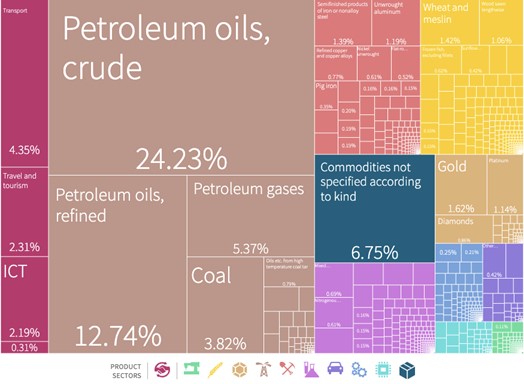

- Export Supply Disruptions. In a similar vein to the above, Russia and Ukraine are also key exporters of various goods that are now not getting to their respective buyers. Oil is the one that most people talk about, but there are several other goods that are also significantly affected. This graph[3] from The Atlas of Economic Complexity shows the specific goods that make up Russia’s export basket and it illustrates the scope of the problem here.

- Commodity Price Inflation. As a result of the supply shortages, prices of key commodities such as gold, platinum, and oil have gone up[4]. This inflation increases the cost of energy and the costs of doing business – all of which has a material impact on the bottom line. This impact is disproportionate for the mining industry because of how big a factor energy costs are within the wider context of the cost base.

Of course, the increased prices do offer some mitigation of this impact because mining companies can sell their goods for more than they previously could, but this effect is muted because of the diminished buying power in the market thanks to the macro-scale inflation that we’re seeing across the world[5].

- Economic and Political Instability. The second-order effects of this conflict on the region’s economic and political instability also play a significant role. Any mining companies who have operations or clientele in the region will be facing significant uncertainty about the future prospects of those deals and this places strain on global mining conglomerates whose assets are stuck in limbo for an undetermined amount of time.

This impact is felt in a wide variety of ways, stretching beyond pure transactional relationships and infiltrating insurance, market risk, currency pressures, and more. All of this adds up to place significant strain on economies that are still recovering from the impact of the COVID-19 pandemic.

These are just some of the key impacts that the mining industry is facing as a result of the conflict. Each of these is incredibly nuanced and interrelated, but hopefully, it gives you a sense of the key factors that are playing a role at the moment.

Now, let’s look forward to some of the potential action steps that can be taken to mitigate this risk and even to benefit from the opportunities that have been presented.

Where To From Here?

It’s nigh-impossible to predict how the months to come will play out, but we can speculate about four principles that are worthy of consideration for the mining industry:

- Opportunities to Address Supply Shortages. Organizations that are well-positioned to service the demand for commodities have an opportunity to seize upon new clients and new markets that they may have not had access to before. This is possible for both developing as well as developed countries to step up and take advantage of the changes in the global supply chain.

- Address Key Supplier Dependence. Mining companies who have been too dependent on specific suppliers for key inputs are now being forced to reckon with the risks that this reliance brings[6]. It’s crucial that companies look to activate secondary supplier relationships that can diversify these risks and offer appropriate solutions in times of difficulty.

- Decreased Reliance on Russian Energy. This conflict has been a wake-up call for much of the Western world that still finds itself too reliant on Russian oil and natural gas. Hopefully, the mining sector can take heed of the risks here and shift its reliance away from the region and toward more stable and sustainable means of procuring energy. Often this will mean moving towards energy independence – especially when you consider how economic sanctions can completely disrupt a globalized supply chain without warning.

Some believe that this shift will be yet another tailwind behind the shift towards renewable energy, but the veracity of this claim is difficult to verify because there is no direct link, short of the oil price increases that are often used as a proxy for the viability of fossil fuels.

- Realignment of Priorities. Events like this provide a valuable moment in time to re-examine one’s assumptions and plot a new path forward if needed. Mining companies who are forward-thinking will use this incident to explore what a mining operation of the future looks like and what key commodities are going to be important for the globe over the long term. This can then inform strategic changes that can transform the prospects of the organization.

Those four pillars are likely to be the key opportunities that mining companies have to transform this crisis into an inflection point that changes the way they do business. This will not come easily, but those companies that can accomplish the requisite shifts will find themselves in a very strong position moving forward.

For as long as this war continues, the market turmoil will continue, and mining will have to roll with the punches. In time we’ll look back with perfect hindsight on what happened, but for now – it’s imperative that we keep our eyes open, monitor our industry carefully, and act decisively to make the most of a terrible situation.

Some Final Thoughts

Some catastrophists have been forecasting a major shortage of all commodities due to Russia’s newly acquired nation non-grata status. Other mining execs may have interpreted the oncoming commodity shortages as an opportunity for windfall profits. Both of these perspectives are likely overstated.

Russia accounts for a 43% of palladium production and 31% of diamond production[7]; two commodities the world can make do without for some time. It is likely the world’s miners can pick up the slack for the remaining commodities as long as demand stays static.

Lastly, we’d like to express our sincere condolences to all those who are being affected by the conflict. We hope that peace prevails sooner rather than later, and we can start to help rebuild all that has been lost.

[1] ‘Russian Invasion of Ukraine: Potential Impact on Supply Chains of Mineral Commodities’ by GlobalData. https://www.mining-technology.com/comment/supply-mineral-commodities/

[2] ‘Value of Palladium Exports from Russia from 2018 – 2020’ from Statista. https://www.statista.com/statistics/1295821/palladium-exports-russia/

[3] Sourced from https://atlas.cid.harvard.edu/countries/186/export-basket

[4] ‘How Russia’s Invasion of Ukraine Rocked Commodity Markets’ by Ashutosh Pandey. https://www.dw.com/en/how-russias-invasion-of-ukraine-rocked-commodity-markets/a-61235041

[5] ‘War in Ukraine Heightens Inflation Risks and Challenges the Global Economy’ by Daniel Solomon and Lan Ha. https://www.euromonitor.com/article/war-in-ukraine-heightens-inflation-risks-and-challenges-the-global-economy

[6] ‘Supply Chain Implications of the Russia-Ukraine Conflict’ by Jim Kilpatrick. https://www2.deloitte.com/uk/en/insights/focus/supply-chain/supply-chain-war-russia-ukraine.html

[7] Russian invasion of Ukraine: Potential impact on supply chains of mineral commodities – Mining Technology (mining-technology.com)